When Soho House agreed to be taken private in a $2.7 billion deal led by MCR Hotels, the headline was about debt relief and an escape from public-market scrutiny. But for industry analysts, the more interesting storyline is what comes next. Freed from quarterly pressures, Soho House may soon look less like a hospitality operator and more like a natural acquisition target for a luxury group such as LVMH Moët Hennessy Louis Vuitton SE.

From IPO Darling to Market Strain

When Soho House—formally Soho House & Co.—went public in 2021, it positioned itself as the first members-only cultural brand on Wall Street. Membership swelled from 119,000 at IPO to more than 200,000 across 46 Houses worldwide. Yet profitability remained elusive.

The stock price declined nearly 40% from its debut, weighed down by high debt and questions over whether cultural cachet could be converted into shareholder returns. Compounding the pressure, Soho House’s reliance on long-term property leases saddled it with heavy fixed costs. While the strategy ensured control of sought-after addresses in London, New York, and Paris, it left the company less agile than asset-light peers such as Marriott or Hyatt, which typically manage or franchise properties owned by outside investors.

By comparison, Belmond—acquired by LVMH in 2018 for $3.2 billion—owned many of its marquee assets outright, from the Hotel Cipriani in Venice to the Venice Simplon-Orient-Express train. That structure provided tangible real estate value and stronger downside protection, underscoring why Soho House’s lease-heavy portfolio appeared riskier to public investors.

Why LVMH Would Care

Why LVMH Would Care

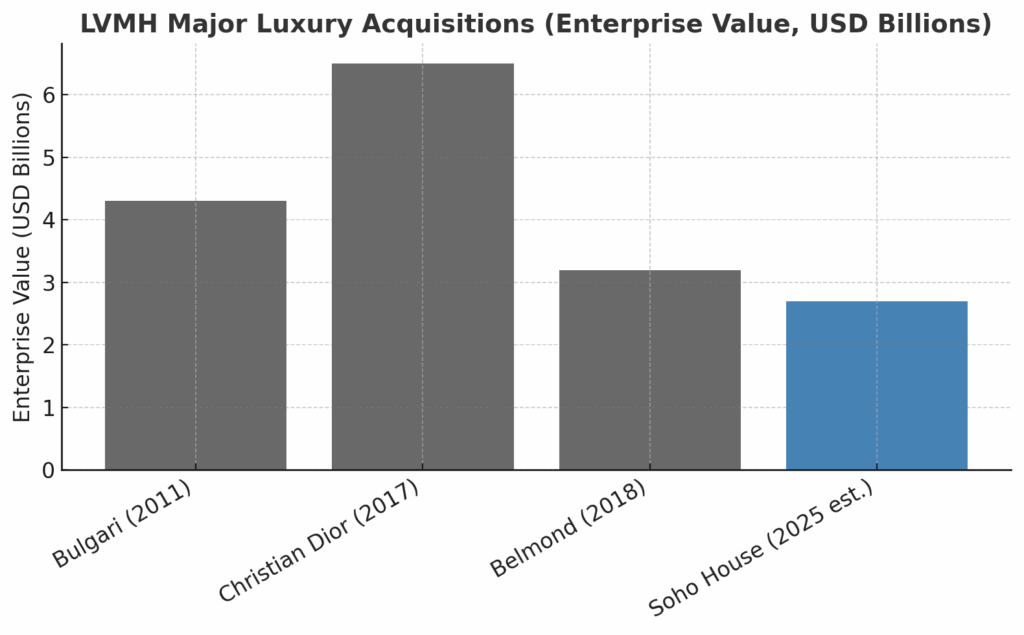

LVMH’s acquisition history shows a growing appetite for luxury experiences:

Belmond (2018): $3.2B EV, giving LVMH a foothold in high-end hospitality.

Christian Dior (2017): €6.5B, consolidating one of its flagship fashion houses.

Bulgari (2011): €4.3B, expanding jewelry and watches.

What LVMH lacks is a membership-based cultural platform. Soho House offers:

Global Footprint: Locations across major creative capitals.

Cultural Cachet: A-list membership overlapping with LVMH’s customer base.

Hospitality Synergy: Hotels, restaurants, spas, co-working, and retail collaborations.

Community as a Product: A monetized sense of belonging—a natural extension of the luxury experience.

“Soho House gives you not just properties—it gives you a pipeline to tastemakers across three continents,” said Zack Bates, private club and luxury hospitality consultant.

The Private Club Boom

The Private Club Boom

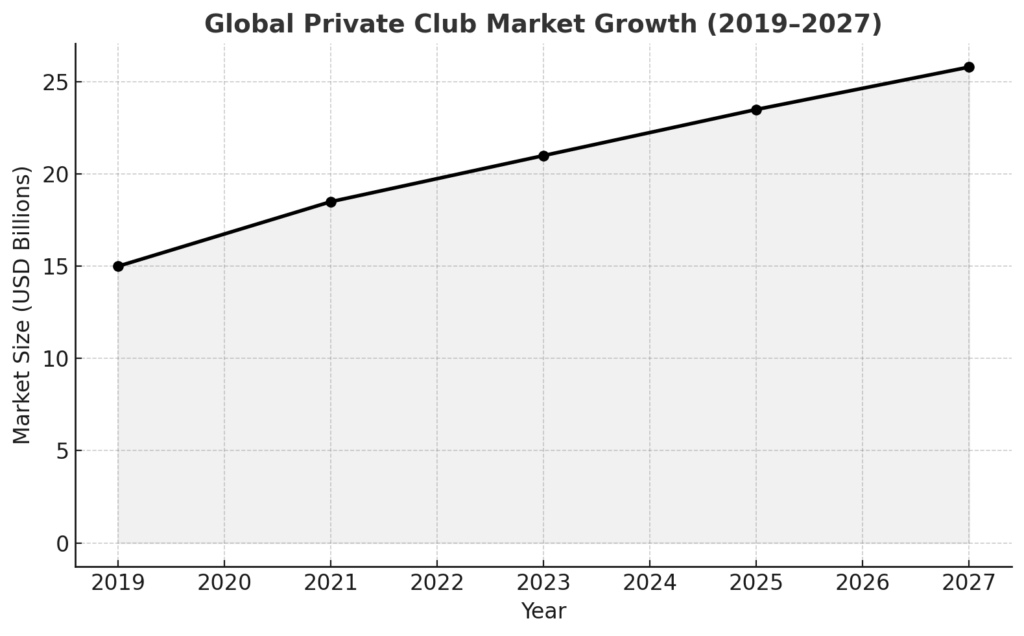

The private-club sector itself is booming:

3,900 U.S. clubs generated $32.6B in direct revenue in 2023.

Industry supports 1.5M jobs and $65B in payroll

Global market projected to reach $25.8B by 2027, with an 11.2% CAGR.

Membership has grown 25% since 2019, with millennials now accounting for ~30% of new golf club members.

At the top end, initiation fees at some Florida clubs exceed $1M.

This aligns with Soho House’s positioning: aspirational, community-driven, and designed for experience-first consumers.

Timing and Execution

The MCR deal, expected to close by the end of 2025, brings new governance—Ashton Kutcher joining the board and Neil Thomson named CFO among the highlights. If Soho House’s private ownership can demonstrate operational efficiency and steady profitability, the company will become a far cleaner acquisition target.

Risks for LVMH

Still, the path is not without obstacles. Soho House’s long-term leases, while ensuring control of prime real estate, create structural costs that could weigh heavily if membership growth slows or consumer spending softens. Unlike Belmond, which provided LVMH with appreciating real estate assets, Soho House would represent a bet primarily on brand equity and recurring membership revenue.

Another challenge is preserving exclusivity at scale. Soho House has expanded rapidly in recent years, and some critics argue that the brand risks diluting its cultural cachet by opening too many locations. For a luxury conglomerate, the question is whether Soho House can maintain its “insider” allure while also justifying its valuation on a global stage.

Finally, integration risk looms. LVMH’s portfolio is built on heritage, craftsmanship, and timeless appeal. Soho House, by contrast, trades on trend, community, and the social lives of a younger demographic. Aligning the two without alienating members—or eroding the brand’s cool factor—would require delicate management.

Outlook

Soho House’s lease-heavy cost structure may have doomed it on public markets, but as a private entity it can refine its model and prepare for the kind of buyer who values exclusivity, culture, and brand halo more than balance-sheet neatness.

For LVMH, the attraction is obvious: Soho House offers a ready-made global community of tastemakers and creatives—the very audience its fashion, jewelry, and hospitality brands aim to court.

In that sense, going private may not be an ending for Soho House, but the prelude to its role in the portfolio of the world’s largest luxury group.